In house financing is a form of dealer financing in which the seller, not a bank or credit union, lends the money to the buyer under a dealer financing agreement, often for people with bad credit. In plain terms, the store or dealer acts as the lender.

That setup can feel simpler than a bank loan, but simple doesn’t always mean cheap. This guide walks through how it works, who may qualify, the main risks, and whether this kind of seller financing makes sense for your budget.

Payment Estimator

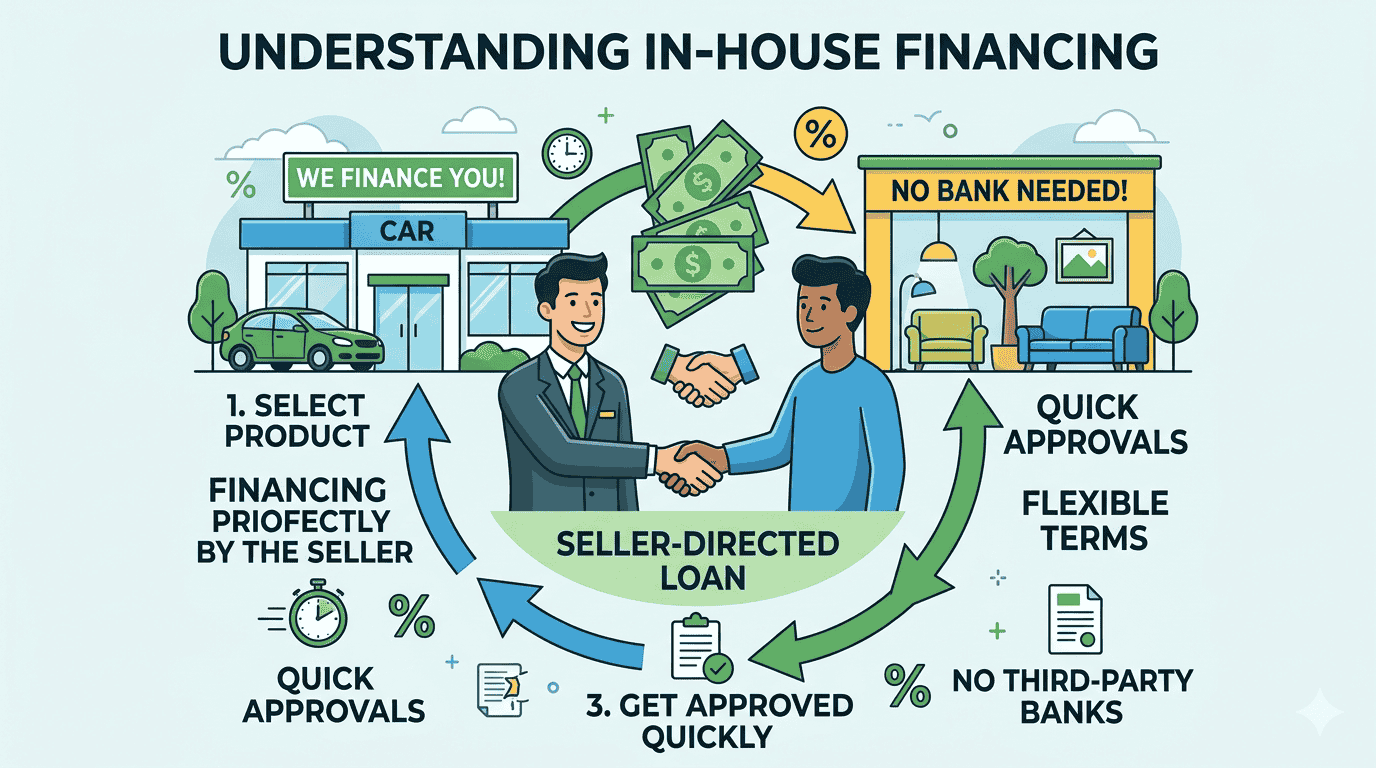

How in house financing works, from application to final payment

With in house financing, you first choose the item, often a car, then apply directly with the seller. Most sellers ask for proof of income, proof of residence, an ID, and a down payment. If approved, you sign a promissory note or loan contract, then follow a set repayment schedule. In many cases, the item itself serves as collateral, so the seller can take it back if you stop paying. For a legal overview, see this consumer-law explanation of auto loan structure.

What lenders usually check before they approve you

Approval often turns on income, job history, housing stability, and basic creditworthiness. Standards are often more flexible than bank rules. Still, the seller wants proof that you can pay on time and keep paying.

What your financing agreement may include

Read the contract line by line. It should show the APR, payment dates, late fees, total loan cost, and any balloon payment. It should also explain what happens after missed payments, including default and repossession.

In house financing vs traditional financing, what changes for the buyer

The biggest difference is who takes the risk. A bank or credit union uses stricter underwriting and usually offers lower costs to stronger borrowers. An in house lender may approve faster because everything happens in one place. That convenience matters, but the full price of the loan matters more. If you want a side-by-side view, this comparison of dealer and bank loans gives a useful snapshot.

Credit requirements are often easier, but that comes at a price

This option can help buyers with thin credit files or past problems. That is why it often appears in ads for bad credit auto loans. Traditional lenders, by contrast, usually want stronger scores, lower debt, and a longer credit history.

Interest rates and total cost can look very different

A manageable monthly payment can hide a costly loan. In 2026, average regular auto loans sit near 6.7% for new cars and 7.1% for used cars. In house financing, by contrast, often carries a much higher interest rate, sometimes 15% to 25% or more, plus extra fees. Over time, that gap can cost thousands.

Approval speed is faster when everything happens in one place

Speed is the main draw. Some sellers can approve a deal the same day with less paperwork. A bank loan may take longer because underwriting is more formal and document-heavy.

Who can qualify, especially if you have bad credit or no credit history

Many sellers look harder at your ability to pay than at your score alone. That makes in house financing appealing when a bank says no. Still, approval is never automatic, and terms can vary a lot from one seller to the next.

In house financing with bad credit, what sellers may look for

A credit manager may review steady income, proof of residence, references, and the size of your cash upfront. A larger down payment can lower the lender’s risk and improve your odds.

No credit check offers, what that claim usually means

Some ads promise no credit check, but that rarely means no review at all. The seller may skip a hard pull yet still verify your income, identity, prior payments, and current obligations before making a decision.

The biggest risks to understand before you sign

Easy approval can feel like a side door when the front bank entrance is closed. Still, that side door may lead to a more expensive room.

Easier approval does not always mean a better deal.

High APR can make a low monthly payment cost much more over time

APR is the yearly cost of borrowing, shown as a percentage. A high APR, plus fees, can turn a modest payment into a much larger total bill than you expected.

Balloon payments can create a hard surprise at the end

A balloon payment is one final payment that is much larger than the others. If your contract includes one, make sure you know the amount and when it comes due.

Repossession can happen faster if you fall behind

When the item is collateral, the seller has stronger rights after default. State rules differ, so read the contract closely and learn how quickly the lender can repossess the vehicle or item.

Some loans may not help you build credit

Not every seller reports on-time payments to the major credit bureaus. That means you could carry high-cost debt and still get little credit-building benefit from it.

Why in house financing is so common for cars

Cars are the most common example because people often need transportation fast. If credit problems block a bank loan, a dealer may offer financing at the lot. That is why this model remains common in used-car sales, including dealer examples tied to bad credit financing.

How dealer-financed car loans usually work

You pick a vehicle, make a down payment, sign the financing papers, and then pay the dealer directly. In a buy here pay here setup, the dealership often handles both the sale and the loan.

When a car buyer may choose this option, and when they should pause

This path may help when you need a car quickly or your credit is damaged. Pause, however, if the vehicle price seems inflated, the rate is steep, or the loan cost far exceeds the car’s value.

How to decide if in house financing is right for you

Treat it like any other loan decision. Compare at least one outside offer, check the full cost, ask whether payments are reported to credit bureaus, and confirm that the repayment schedule fits your cash flow. If the payment only works on paper, the deal is too tight.

Green flags that suggest the deal may be fair

Clear terms, a stated APR, reasonable fees, and flexible payment dates are good signs. So is a seller who answers questions directly and gives you time to review the paperwork.

Warning signs that mean you should walk away

Pressure to sign fast, vague charges, missing documents, or a plan built around a future lump sum are all red flags. If the numbers are hard to follow, step back.

Common questions about in house financing

Does in house financing affect your credit?

It can, but only if the seller reports to the credit bureaus. Missed payments may still hurt you through collections or later loan applications, even when positive payments are not reported.

Can you refinance in house financing later?

Yes, some buyers refinance later with a bank or credit union. That often happens after several on-time payments or once credit improves enough to qualify for a lower rate.

How does in house financing work for cars?

The dealer sells the car and provides the loan. You make a down payment, sign the contract, and then pay the dealer over time under the agreed schedule.

Is in house financing the same as buy here pay here?

Not always, but they overlap. Buy here pay here is a common car-dealer version of in house financing, where the dealership handles both the sale and the lending.

Do you need a down payment for in house financing?

Often, yes. Many sellers ask for one to lower their risk. A larger amount upfront may also reduce the monthly payment or improve your approval chances.

Is no credit check in house financing a good idea?

It can help some buyers get approved. Still, those deals may come with higher rates, stricter terms, or faster repossession rights, so the contract deserves close review.

In house financing can help when fast approval matters or when bad credit financing is your only near-term option. Still, the financing agreement, the interest rate, and the repossession terms matter more than convenience.

Before you sign, compare at least one outside loan offer. A little extra time can save a lot of money.